When a new financial service enters the Pakistani market, scepticism is healthy. It's the job of CFOs, compliance officers, and HR leaders to ask hard questions before adopting any solution that touches employee compensation.

Earned Wage Access (EWA) is no exception. In fact, it's often misunderstood, confused with loans, salary advances, or worse, predatory lending schemes. This confusion isn't just semantics. It affects whether companies adopt a tool that could genuinely improve employees' financial wellness or dismiss it out of caution.

So let's clear the air. Here are the most common EWA myths in Pakistan, and what the facts actually say.

The Reality: EWA is not a loan. Full stop.

A loan involves borrowing money you haven't earned yet. It comes with repayment terms, interest (or markup), and the risk of default. EWA is fundamentally different. It provides employees access to wages they have already earned but haven't yet been paid because of the monthly payroll cycle.

Think of it this way: if an employee works 15 days of the month, they've earned 15 days of salary. EWA simply allows them to access a portion of that amount before the end of the month, without borrowing, without interest, and without creating debt.

This distinction matters. When evaluating whether EWA is a loan, the answer is clear: no. There is no principal to repay, no interest accruing, and no loan agreement. It's a liquidity tool, not a credit product.

The confusion is understandable, but important

Many Pakistani companies already offer salary advances to employees in emergencies. So, how is EWA different?

Salary advance vs earned wage access comes down to three key factors: structure, oversight, and sustainability.

Salary Advance:

Earned Wage Access:

The distinction isn't trivial. One is reactive and inconsistent. The other is proactive, structured, and scalable. A responsible, safe salary advance model should include transparency, caps, and education, features that modern EWA platforms provide by design.

The fear: If employees can access their salary early, they'll spend recklessly and fall into a cycle of dependency.

The reality: Responsible EWA models are designed to prevent this, not enable it.

Here's how:

Debt traps occur when people borrow more than they can repay, with interest compounding over time. EWA avoids this entirely because it's not borrowing at all. It's accessing money already earned.

The concern: Adding a new system that touches employee compensation sounds complicated. Will it mess with payroll cycles? Create reconciliation issues? Add costs or administrative burden?

The reality: EWA is designed to integrate seamlessly with your existing payroll—not replace or complicate it.

Here's how responsible EWA platforms like Neem Paymenow work in practice:

In truth, EWA is simple, seamless, and designed to work with your existing payroll, not against it.

The concern: New fintech solutions, particularly those involving payroll, raise concerns about data security, compliance, and regulatory oversight.

The reality: Reputable EWA providers operate within the same compliance and security frameworks as other financial services.

For Neem Paymenow specifically:

While Pakistan's EWA regulatory landscape is still evolving, responsible providers prioritise transparency, compliance, and ethical design. Employers evaluating EWA should ask hard questions about how the platform operates, who owns employee data, and how the service aligns with labour laws and Shariah principles.

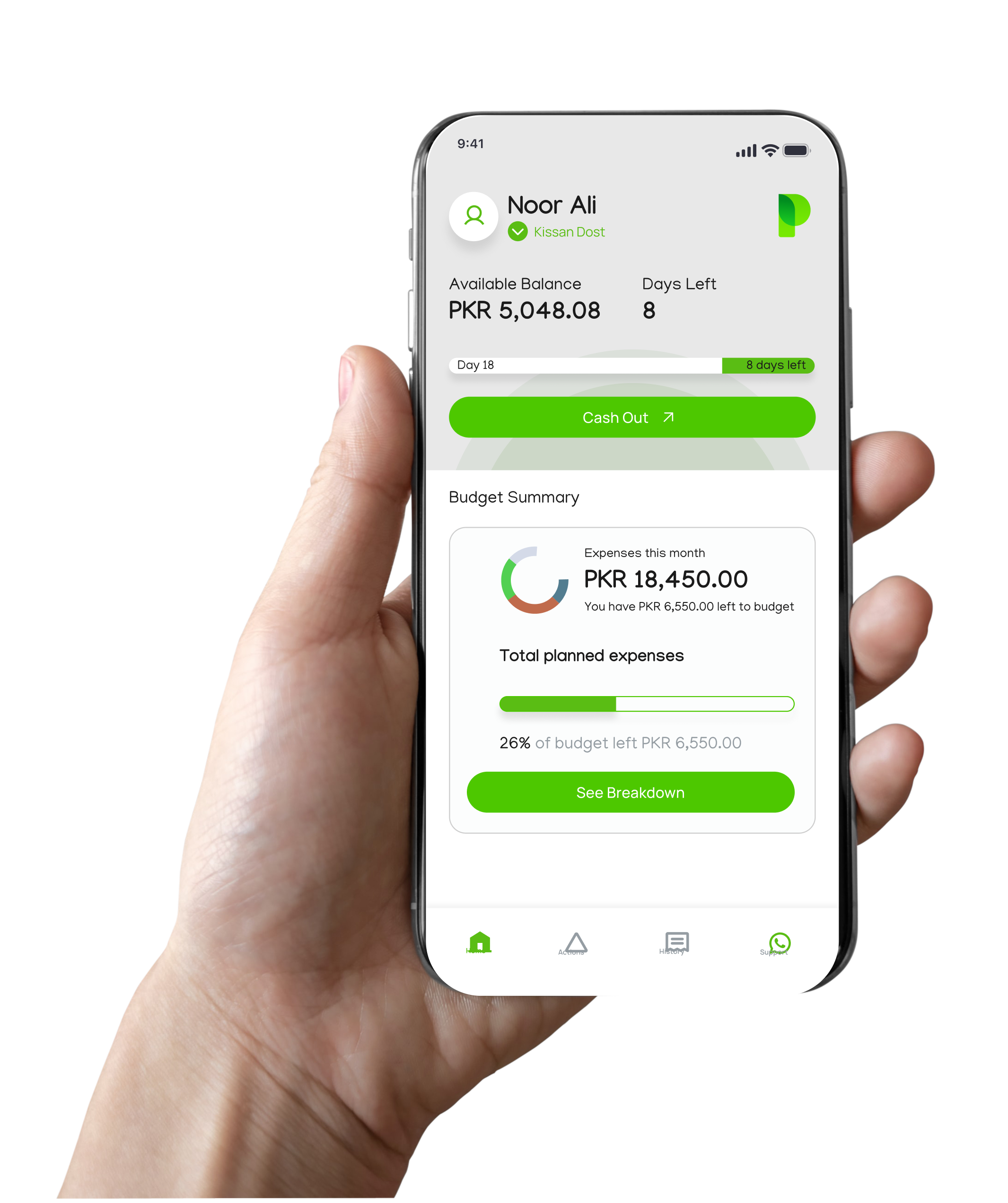

At its core, Earned Wage Access is a tool that bridges the gap between when employees earn their salary and when they receive it.

Here's how it works in practice with Neem Paymenow:

No loan. No debt. No long-term liability. Just flexible access to money they've already earned.

For HR leaders and CFOs, the appeal of EWA isn't just employee satisfaction (though that's significant). It's also operational.

Earned Wage Access is not a loan, not a traditional salary advance, and not a debt trap. When implemented responsibly, with caps, oversight, and financial education, it's a safe, transparent way to give employees more control over their earnings.

The confusion around EWA is understandable. It's a new model in Pakistan, and healthy scepticism is warranted. But the facts speak for themselves. EWA, done right, is a financial wellness tool that benefits employees and employers alike.

At Neem Paymenow, we've built more than just an EWA solution, we've created a Shariah-compliant, SECP-certified financial wellness platform designed specifically for Pakistan. With seamless payroll integration, robust data protection, and in-app financial education (available in both English and Roman Urdu), we're helping employees not just access their earnings early, but build long-term financial resilience.

If your organisation is exploring safe salary advance options or evaluating fintech solutions for financial wellness, the key is to ask the right questions. How is the platform structured? What safeguards are in place? Is it compliant with Shariah and local regulations?

At Neem Paymenow, we believe transparency and responsibility aren't optional; they're essential. Because employee financial wellness isn't just about access, it's about access done right.

Ready to explore EWA for your team? Neem Paymenow offers a free consultation to provide a walkthrough on how earned wage access integrates with your payroll, what safeguards we include, and how other Pakistani companies are implementing it responsibly.

FROM THE BLOG

.png)

%20(1).png)

.png)

.png)